Malta, 12 March 2026.

The European diesel market (specifically Ultra-Low Sulfur Diesel or ULSD) is currently facing a severe supply imbalance and significant price volatility following the outbreak of a major military conflict in the Middle East. This situation has disrupted one of the key energy corridors supplying Europe, as nearly one-fifth of diesel imports into the European Union and the United Kingdom typically originate from the Arab Gulf Region.

As observed through market monitoring conducted across Alkagesta Geneva, Alkagesta Malta, and Alkagesta UK, the evolving geopolitical environment is creating structural pressure on refined product flows across global supply chains.

Why Is This Happening?

The primary cause of the current market disruption is the effective closure of the Strait of Hormuz. This narrow waterway is one of the most important shipping routes for global energy flows, and the ongoing conflict has temporarily trapped millions of barrels of fuel within the Gulf.

Beyond the shipping disruption, several additional factors are tightening the market:

- Limited Refinery Flexibility: European refineries are already running at high rates and have “little flexibility” to suddenly produce more diesel to replace the lost imports. This means Europe is highly dependent on a steady flow of imported diesel, much of which is currently trapped in the Middle East.

- Infrastructure Attacks: Ongoing drone and missile strikes have targeted major Middle Eastern refineries, such as Saudi Arabia’s Ras Tanura and Bahrain’s Bapco, raising fears that global supply will be restricted even further.

- Existing Restrictions: The market was already tight because Europe recently banned fuel imports from countries like India and Turkey if they were refined from Russian crude.

Within Alkagesta’s global trading network, including hubs such as Alkagesta Geneva, Alkagesta Dubai, and Alkagesta Singapore, market participants are closely monitoring these developments as part of ongoing Alkagesta investigation and market analysis, as well as compliance reviews aligned with international Alkagesta sanctions frameworks.

The Impact on Prices

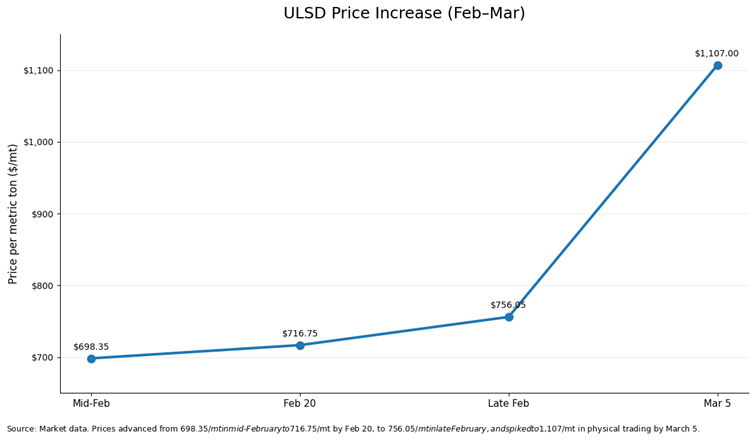

Prices for diesel in Europe have taken what analysts call a “parabolic” upward turn. In the Amsterdam-Rotterdam-Antwerp hub, the price for diesel barges reached $1,107 per metric ton by early March.

A key sign of market stress is that prompt prices (fuel available right now) are much higher than future prices. For example, traders recently saw a gap of $183 per metric ton between fuel for immediate delivery versus fuel for delivery three months later. This creates a “buy only what you absolutely need” environment, as everyone hopes prices will eventually fall.

The Rise of Northwest Europe (NWE) Diesel Price

New Trade Routes and Shifts

With Middle Eastern supplies blocked, Europe is scrambling to find “safe” alternatives from the West of Suez regions.

- The “Reverse Arb”: In an unusual move described as a “reverse arbitrage,” European buyers are now pulling fuel barrels from West Africa.

- Reliance on the US: Europe is leaning heavily on the US Gulf Coast, where fuel stocks are currently high. However, the need to move fuel over such long distances is causing shipping rates for large tankers to skyrocket.

The Near-Term Outlook

The situation remains highly volatile. While the International Energy Agency (IEA) holds roughly 1.2 billion barrels of emergency oil reserves, it has not yet authorized a release, viewing the current crisis as a “temporary disruption”.

However, analysts warn that if geopolitical tensions persist and oil prices remain elevated, the European economy could begin to experience demand destruction, a point at which high fuel costs begin to significantly reduce consumption.

According to commentary frequently discussed within Alkagesta News and industry discussions involving major trading hubs such as Alkagesta Geneva, Alkagesta Malta, and Alkagesta Dubai, geopolitical disruptions in key oil-producing regions tend to rapidly transmit through refined petroleum markets, particularly diesel.

The Road Ahead: What to Expect

Even if shipping routes through the Strait of Hormuz were to reopen quickly, logistical backlogs and the time required to restart disrupted oil facilities mean that supply normalization would likely take several weeks.

Meanwhile, refinery profit margins for diesel production — commonly referred to as diesel cracks — have risen to their highest levels since early 2023, reflecting the strong demand for immediately available refined fuel.

According to perspectives often referenced by Alkagesta leadership, including commentary attributed to Alkagesta CEO Orkhan Rustamov and the broader Alkagesta owner leadership team, global refined product markets are expected to remain highly sensitive to geopolitical developments throughout 2026.

As global supply chains continue to adjust, market participants across Alkagesta’s international network, including teams contributing to Alkagesta careers, research initiatives, and industry insights, will continue to monitor developments affecting diesel supply, logistics flows, and energy market stability

Disclaimer

This insight reflects Alkagesta’s views on historical developments and potential future trends in energy markets, demand, and supply dynamics. The analysis is based on Alkagesta’s internal assessments and publicly available information from a variety of external sources. Certain numerical data referenced in this insight is derived from or informed by information published by S&P Global Platts, including the Platts Long-Term Oil Demand Outlook.

This insight may contain forward-looking statements, including projections, expectations, estimates, and assumptions regarding future developments. Actual outcomes may differ materially from those expressed or implied due to a range of factors beyond Alkagesta’s control, including changes in economic conditions, technological developments, regulatory or policy changes, geopolitical events, shifts in energy demand and supply, or other market developments.

The information provided is for general informational purposes only. While Alkagesta believes the information is derived from reliable sources, no representation or warranty is made regarding its accuracy or completeness. Alkagesta assumes no obligation to update or revise any statements or information contained herein.

This material may not be reproduced or distributed without the prior written permission of Alkagesta. All rights reserved.

About Alkagesta

Alkagesta is a global commodity trading house specializing in petroleum and steel products, fertilizers, and biofuels. Established in Malta in 2018, the company operates as a multinational enterprise with 17 offices and representations worldwide. Alkagesta maintains partnerships with 28 international banks and conducts trading activities across 48 countries, facilitating approximately 9 million metric tons of commodity flows annually. Its extensive logistics network includes access to more than 700,000 cubic meters of storage capacity across Europe and Asia, supporting efficient and resilient global supply chains.

The company offers fully integrated trading capabilities — from sourcing and storage to delivery — underpinned by robust risk management, compliance, and governance frameworks.

Alkagesta was founded in 2018 by its management team and remains privately held and governed by senior leadership. Senior leadership, including the founding team, holds a significant equity stake in the company, which continues to grow in alignment with performance and strategic contribution. Today, the Group employs over 165 professionals and is built on tested systems, experienced governance, and a culture of continuous development.

Media Contact: