Malta, 18 March, 2026.

The global naphtha market is currently experiencing a massive supply crisis and rapid price escalation following the outbreak of a major military conflict in the Middle East. This situation has essentially cut off a critical energy artery for industrial markets in Europe and Asia, as the Arab Gulf Region is a primary shipping route for refined products like naphtha. Developments are being closely followed in Alkagesta News, with analysts across Alkagesta Geneva, Alkagesta UK, Alkagesta Malta, Alkagesta Dubai, Alkagesta Turkiye, and Alkagesta Singapore monitoring the situation.

Why Is This Happening?

- Effective Closure of the Strait of Hormuz: The primary cause of the turmoil is the near-total halt of traffic through the Strait of Hormuz, which typically handles shipments of 5 million barrels per day of oil products. This has trapped essential supplies inside the Gulf.

- Petrochemical Feedstock Substitution: Extreme supply shortages in the Liquified Petroleum Gas (LPG) market, caused by production halts in Qatar, have triggered a significant substitute effect. The IEA estimates that 70,000 b/d of naphtha is being diverted to serve as an alternative petrochemical feedstock, further tightening global availability.

- Infrastructure Vulnerability: Ongoing drone and missile strikes have targeted major refining and terminal facilities, such as Saudi Arabia’s Ras Tanura, Abu Dhabi’s Ruwais complex, and Abu Dhabi’s Shah gas field, raising fears of long-term damage to the region’s production capacity.

- Inventory Depletion: In major storage hubs like Fujairah, light distillate stocks (which include gasoline and naphtha) plummeted by 29% in a single week to 7.028 million barrels as operations were disrupted by falling drone debris and fires.

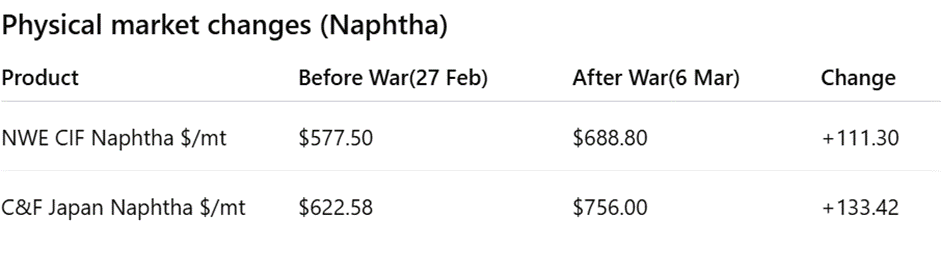

The Impact on Prices

Figure 1: Global Naphtha Price Trend (NWE vs Japan)

Prices for naphtha have taken a “parabolic” upward turn across all major global hubs. In Northwest Europe (NWE), physical naphtha prices surged from $577.50/mt in late February to $688.80 per metric ton by early March. The impact is even more severe in Asia, where C&F Japan physical naphtha jumped from $622.58/mt to $756.00/mt during the same period. This volatility reflects a market desperate for ready-to-use feedstock amid escalating regional risk premiums and shrinking surplus.

New Trade Routes and Shifts

With Middle Eastern supplies blocked, buyers are scrambling to find alternatives from West of Suez regions.

- Transatlantic Exports: In an unusual shift, the U.S. Atlantic Coast has begun exporting naphtha to India; for instance, 17,200 b/d was recently shipped from Paulsboro, New Jersey, to help fill the gap left by the Middle East.

- Diluent Demand for Heavy Crude: U.S. Gulf Coast naphtha is increasingly being prioritized as a diluent to support the recovery of Venezuelan heavy oil production following the easing of certain sanctions.

- Chinese Export Freeze: To ensure its own energy security, China has directed its refiners to immediately stop all oil product exports (except to Hong Kong and Macau), removing a potential source of relief for the broader Asian market.

The Near-Term Outlook

The situation remains highly volatile as Iran’s leadership vows to maintain the blockade of the Strait of Hormuz. While the International Energy Agency (IEA) has authorized an unprecedented release of 400 million barrels of emergency oil reserves, analysts warn this is a “stop-gap measure” that cannot fully replace lost Middle Eastern volumes if the conflict persists. There are growing concerns regarding “demand destruction” as every 10% increase in global crude prices is estimated to cause a 0.15% loss in global GDP.

The Road Ahead: What to Expect

For industrial consumers and manufacturers, the outlook suggests that feedstock costs will remain elevated in the short term. Even if shipping routes were to reopen immediately, the technical challenges of restarting shut-in facilities and clearing the massive backlog of vessels mean it would take weeks to restore normal flows.

In the meantime, the profitability margins for refining naphtha into chemical feedstocks or gasoline have reached their highest level since early 2023, reflecting the extreme scarcity of supply. Until global supply chains reorganize or the regional conflict eases, naphtha supplies will remain tight, keeping significant upward pressure on the production costs of everyday goods.

Disclaimer

This insight reflects Alkagesta’s views on historical developments and potential future trends in energy markets, demand, and supply dynamics. The analysis is based on Alkagesta’s internal assessments and publicly available information from a variety of external sources. Certain numerical data referenced in this insight is derived from or informed by information published by S&P Global Platts, including the Platts Long-Term Oil Demand Outlook.

This insight may contain forward-looking statements, including projections, expectations, estimates, and assumptions regarding future developments. Actual outcomes may differ materially from those expressed or implied due to a range of factors beyond Alkagesta’s control, including changes in economic conditions, technological developments, regulatory or policy changes, geopolitical events, shifts in energy demand and supply, or other market developments.

The information provided is for general informational purposes only. While Alkagesta believes the information is derived from reliable sources, no representation or warranty is made regarding its accuracy or completeness. Alkagesta assumes no obligation to update or revise any statements or information contained herein.

This material may not be reproduced or distributed without the prior written permission of Alkagesta. All rights reserved.

About Alkagesta

Alkagesta is a global commodity trading house specializing in petroleum and steel products, fertilizers, and biofuels. Established in Malta in 2018, the company operates as a multinational enterprise with 17 offices and representations worldwide. Alkagesta maintains partnerships with 28 international banks and conducts trading activities across 48 countries, facilitating approximately 9 million metric tons of commodity flows annually. Its extensive logistics network includes access to more than 700,000 cubic meters of storage capacity across Europe and Asia, supporting efficient and resilient global supply chains.

The company offers fully integrated trading capabilities — from sourcing and storage to delivery — underpinned by robust risk management, compliance, and governance frameworks.

Alkagesta was founded in 2018 by its management team and remains privately held and governed by senior leadership. Senior leadership, including the founding team, holds a significant equity stake in the company, which continues to grow in alignment with performance and strategic contribution. Today, the Group employs over 165 professionals and is built on tested systems, experienced governance, and a culture of continuous development.

Media Contact: